Selling Your House Before Bankruptcy in Hamilton: What You Need to Know

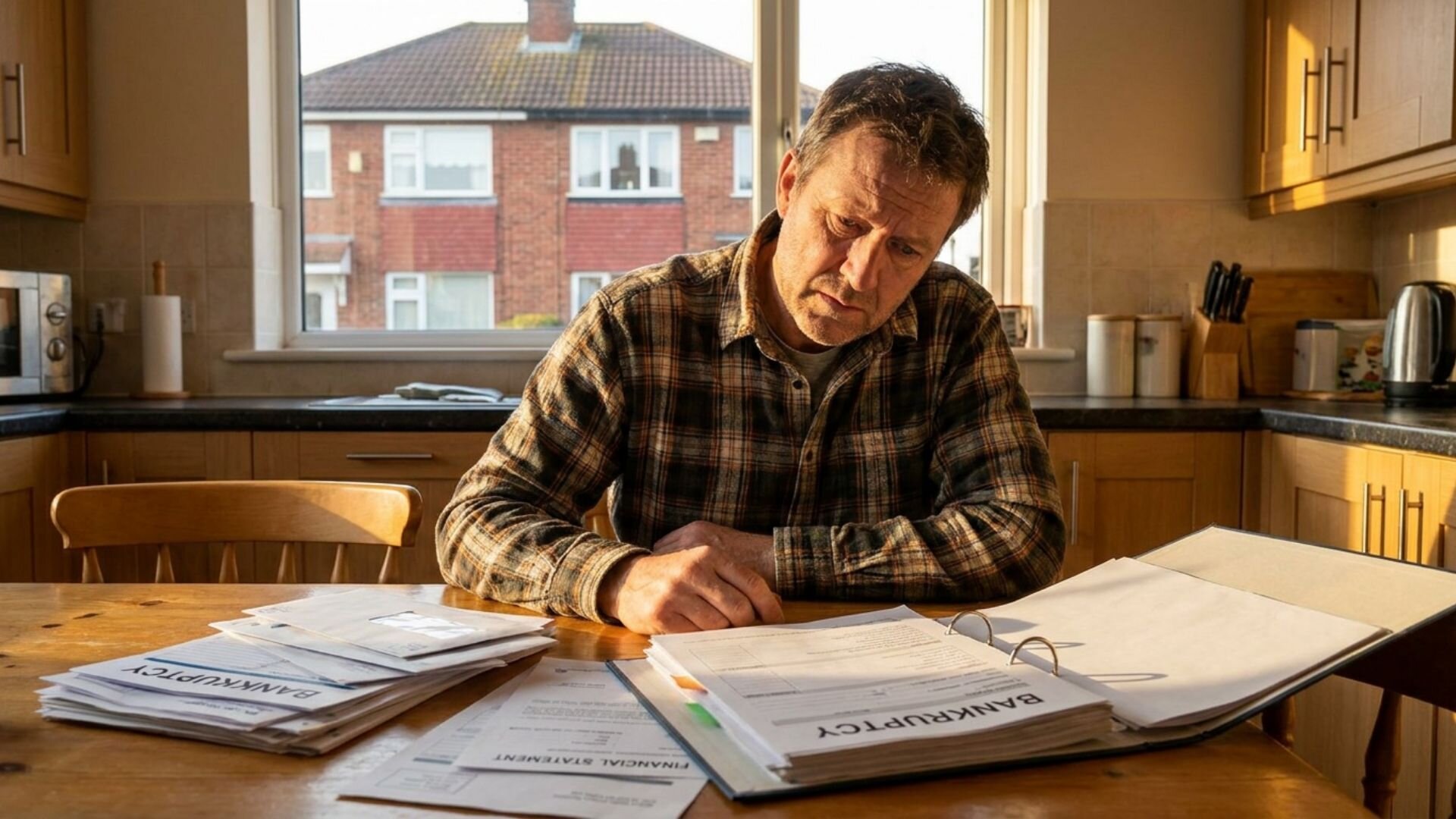

If you’re staring down the reality of bankruptcy in Hamilton, you’re probably asking the same question I hear from homeowners all the time: “Should I sell my house before I file, or will the trustee take it anyway?”

My name is Cassie, and I work with Hamilton House Buyers. Over the years, I’ve sat at kitchen tables across this city — in Stoney Creek, Crown Point, Dundas, Binbrook, and everywhere in between — talking with families who are facing some of the most difficult financial moments of their lives. Bankruptcy is one of those moments. It’s scary, it’s confusing, and when your home is involved, it can feel absolutely overwhelming.

The good news: you often have more options than you think. In many cases, selling your home before filing for bankruptcy in Hamilton is not only possible — it’s one of the smartest financial moves you can make. This guide will walk you through exactly what that process looks like, how it protects you, and how a cash sale can get you out from under crushing debt faster than you ever imagined.

Why Bankruptcy Happens to Good People in Hamilton

Let me say this plainly: bankruptcy is not a character flaw. It’s a legal tool designed to give people a fresh start when debt becomes unmanageable. In Hamilton, I’ve seen it happen to homeowners for all kinds of reasons — a job loss at one of the steel plants on Barton Street East, a medical crisis that drained savings, a separation that split one income into two households, or a small business that couldn’t survive the economic headwinds of the past few years.

According to the Office of the Superintendent of Bankruptcy Canada, Ontario consistently leads the country in consumer insolvency filings. The Hamilton-Burlington census metropolitan area sees hundreds of personal bankruptcies and consumer proposals filed every year. Many of those filers own homes — and many of them didn’t know they had other options.

If you own a home and you’re considering bankruptcy, the single most important thing you can do right now is get informed before you file.

What Happens to Your Home if You File for Bankruptcy in Ontario?

In Ontario, when you file for bankruptcy, a Licensed Insolvency Trustee (LIT) is appointed to administer your estate. The trustee’s job is to identify assets that can be sold to repay your creditors. Your home — unless it has little to no equity — is considered an asset.

Here’s how it works in practice:

Ontario’s Execution Act provides a homestead exemption of only $10,000 on your principal residence. That means if your home on, say, Queenston Road in East Hamilton has $80,000 in equity, the first $10,000 is protected — but the remaining $70,000 can be claimed by your trustee for distribution to creditors.

In practical terms, what this means is:

- If your home has significant equity, the trustee will likely sell it to pay your debts.

- You lose control of the timing and the sale price — the trustee will list it on MLS and sell at whatever the market will bear.

- You may receive the $10,000 exemption but nothing more from the proceeds.

- The process can take months, leaving you in limbo.

This is why so many Hamilton homeowners I speak with choose to sell before filing. Selling first puts you in the driver’s seat.

The Case for Selling Before You File: Taking Back Control

Selling your home before filing for bankruptcy gives you several critical advantages:

1. You Control the Process

Once you file, your trustee controls the sale of your home — not you. That means they choose the agent, set the timeline, and ultimately decide what’s acceptable. Pre-bankruptcy, you call the shots. You can choose a cash buyer like Hamilton House Buyers, close in as little as 7–14 days, and use the proceeds to negotiate with creditors or pay off debts entirely — potentially avoiding bankruptcy altogether.

2. You Can Potentially Avoid Bankruptcy Entirely

This is the outcome I love most. I’ve worked with homeowners in Hamilton’s North End, Concession Street neighbourhoods, and out in Waterdown who used the equity from a quick cash sale to settle their most pressing debts — credit card balances, CRA arrears, unsecured loans — and never had to file at all. If your debts are primarily secured against your home or manageable with a lump sum, a fast sale might give you the fresh start you need without the seven-year credit impact of a bankruptcy.

3. You Protect Your Equity

As I mentioned, Ontario only protects $10,000 of your home equity in bankruptcy. If you have $100,000 in equity, you lose $90,000 of it to creditors through the bankruptcy process. By selling on your own terms first, you receive the full equity (minus selling costs), and you direct where that money goes.

4. You Avoid the Credit Damage of Bankruptcy

A bankruptcy in Canada stays on your credit report for six to seven years after discharge for a first-time bankruptcy. A consumer proposal stays for three years after completion. Selling your home and settling debts directly is far less damaging to your long-term financial health.

Ready to sell your house fast in Hamilton?

Or call us directly: (647)-800-4508

Is It Legal to Sell Your Home Before Filing for Bankruptcy?

This is a question I get asked all the time — and the answer is yes, with important conditions.

It is completely legal to sell your home before filing for bankruptcy, provided:

- You sell at fair market value. Selling your home for less than it’s worth to a family member, friend, or anyone else in an attempt to shield assets from creditors is considered a fraudulent preference or fraudulent conveyance under the Bankruptcy and Insolvency Act (BIA). A trustee can unwind these transactions if they occurred within a certain period before filing (generally one to five years, depending on the relationship).

- You use the proceeds appropriately. You can — and should — use sale proceeds to pay off secured creditors (your mortgage lender), CRA arrears, and other debts. You cannot simply give the money away or hide it.

- You disclose the sale to your trustee. If you sell and then file within a year, the trustee will review the transaction. An arm’s length sale at market value will not be reversed.

Selling to an established cash buyer like Hamilton House Buyers is an arm’s length transaction at a fair price — exactly the kind of sale that holds up to trustee scrutiny. We’re not a family member. We’re not a friend. We’re a local business that pays fair cash value for homes in Hamilton and surrounding areas, and we can close on your timeline.

The Typical Timeline: Selling Before Bankruptcy in Hamilton

When you’re facing insolvency, time matters. Here’s what a typical pre-bankruptcy home sale timeline looks like when you work with a cash buyer:

Day 1: You reach out to Hamilton House Buyers and share basic details about your home — location, condition, your situation.

Days 2–3: We visit your property (often a quick walkthrough in neighbourhoods like Rosedale, Homeside, or Stipley) and prepare a no-obligation cash offer. No repairs required. No cleaning. No staging.

Days 4–7: You review the offer and consult with your lawyer or Licensed Insolvency Trustee if you’ve already engaged one. You decide whether to accept.

Days 8–14: If you accept, we handle all paperwork and coordinate with your real estate lawyer. Closing can happen in as little as 7 days from acceptance, or we can give you more time if you need it.

Close of transaction: Proceeds are paid to your lawyer in trust, who pays out your mortgage, any property tax arrears, and other registered liens. Remaining equity goes to you.

Compare that to a traditional MLS listing (45–90+ days in the current Hamilton market) or a trustee-controlled sale (which can take 3–6 months after filing). Speed matters when creditors are calling and interest is compounding.

What About a Consumer Proposal? Can You Still Sell?

Many Hamilton homeowners facing financial distress pursue a consumer proposal instead of bankruptcy. A consumer proposal is an agreement with your creditors — administered by a Licensed Insolvency Trustee — where you pay back a portion of what you owe over up to five years, in exchange for protection from collection actions.

If you’re considering a consumer proposal, your home is generally protected as long as you continue making mortgage payments and keep up with proposal payments. You don’t necessarily have to sell. However, many people choose to sell their home as part of the proposal process to fund a lump-sum settlement, which can:

- Get creditors paid off faster (often at a significant discount)

- Reduce your monthly obligations

- Allow you to rent and rebuild your credit without the burden of a home you can no longer afford to maintain

If you’re weighing these options, I strongly recommend speaking with a Licensed Insolvency Trustee in Hamilton before making any decisions. Organizations like Grant Thornton, MNP Debt, and Hoyes Michalos all have offices in the Hamilton area.

What If You’re Already Behind on Your Mortgage?

Many homeowners who reach out to me are already 30, 60, even 90 days behind on their mortgage. Some have received demand letters or are worried about power of sale proceedings starting. This situation is stressful — but it’s also one where acting quickly can make all the difference.

If your lender has initiated or threatened power of sale proceedings in Hamilton, you typically still have time to sell before the lender forces a sale. In Ontario, the power of sale process has mandatory redemption periods — often 35–45 days after a notice of sale — giving you a window to sell on your terms before the bank takes over.

Similarly, if you’ve accumulated liens on your Hamilton property — from construction holdbacks, CRA tax debts, or court judgments — those liens don’t have to stop a sale. They’ll simply be paid out of the proceeds at closing, just like your mortgage. We work with these situations regularly.

Real Stories from the Hamilton Community

I want to share a few situations (with details changed for privacy) that reflect what I see in this community:

A homeowner on Cannon Street East in the Crown Point neighbourhood called me last winter. He’d lost steady employment after a workplace injury and had racked up nearly $60,000 in credit card debt trying to keep up with his mortgage and living expenses. He was days away from filing for bankruptcy. We made a cash offer on his semi-detached home, closed in 11 days, and he walked away with enough equity to pay off every unsecured creditor in full — no bankruptcy filed, credit intact.

A woman in Ancaster had been through a difficult separation and was left with the family home and a mortgage she couldn’t carry on one income. She’d consulted with a trustee who told her bankruptcy might be inevitable. We bought her home for cash within two weeks. The sale proceeds covered her mortgage and a significant portion of her credit card debt, and she filed a consumer proposal for the remainder — a far less damaging outcome than full bankruptcy.

A couple on the Mountain — near Upper Wentworth — had medical debts and CRA arrears totalling over $90,000. They had equity in their home but were afraid to sell because they didn’t know how the money would work out. After walking through the numbers together, they realized a cash sale would net enough to pay the CRA in full (stopping penalties and interest), clear most of their other debts, and fund a fresh start renting in the east end near Confederation Park.

These aren’t edge cases. This is what financial distress looks like in Hamilton — and these are the outcomes that are possible when homeowners take action early, before bankruptcy is their only option.

What to Do Right Now if You’re Considering Bankruptcy

If you’re a Hamilton homeowner considering bankruptcy, here’s what I recommend as an immediate action plan:

Step 1: Get a free cash offer on your home. Before you file anything, know what your home is worth in a fast cash sale. This takes 24–48 hours and costs you nothing. It gives you the most important number in your financial picture.

Step 2: Talk to a Licensed Insolvency Trustee. Initial consultations with LITs in Ontario are free. They will help you understand whether bankruptcy, a consumer proposal, or debt negotiation is the right path — and how a home sale factors in.

Step 3: Talk to a real estate lawyer. A lawyer can help you understand the legal implications of selling before filing, ensure your transaction is above board, and make sure sale proceeds are distributed correctly.

Step 4: Act quickly. The longer you wait, the fewer options you have. If you’re already behind on your mortgage, interest and penalties are compounding. If creditors are considering legal action, a judgment or lien registered against your property complicates the picture. The best time to act is now.

If you’re experiencing job loss or broader financial hardship in Hamilton, many of the same strategies apply — and you may be surprised how much flexibility a fast cash sale can create in your situation.

Ready to sell your house fast in Hamilton?

Or call us directly: (647)-800-4508

Frequently Asked Questions About Selling Before Bankruptcy in Hamilton

Can I sell my house to pay off debt and avoid bankruptcy?

Yes. If your home has enough equity to cover your debts, or a significant portion of them, selling before filing can help you avoid bankruptcy entirely. Many Hamilton homeowners use a fast cash sale to pay off secured debts (mortgage, CRA) and negotiate settlements with unsecured creditors. The outcome depends on how much equity you have versus how much you owe.

How quickly can I sell my house in Hamilton if I’m facing bankruptcy?

With Hamilton House Buyers, we can close in as little as 7 days. We buy homes as-is, with no inspections, repairs, or agent commissions required. If you need a few more weeks to find alternate housing or consult with advisors, we can work with that timeline too. Most of our transactions close in 10–21 days.

What happens to my mortgage when I sell before bankruptcy?

Your mortgage is paid out at closing from the sale proceeds, just like in any real estate transaction. If your home sells for more than you owe (including mortgage, any registered liens, and closing costs), the remaining equity comes to you. If your mortgage is higher than the sale price — a rare situation in Hamilton’s current market — you’d need to discuss shortfall options with your lender before closing.

Will a trustee reverse my home sale if I file for bankruptcy shortly after selling?

A trustee can only reverse a sale if it was made at an undervalue (below market price) or as a fraudulent preference (to benefit a related party over creditors). An arm’s length sale at fair market value — the kind we complete — cannot be reversed. We recommend keeping all documentation and working with a lawyer to ensure the transaction is clean.

Do I need to tell the bankruptcy trustee about the sale?

Yes. If you sell your home and then file for bankruptcy within a year (or in some cases up to five years for related-party transactions), the trustee will review the sale. Full disclosure is required. This is not something to be afraid of — a legitimate market-value sale to an independent buyer will pass scrutiny.

Can I sell if there are tax liens or judgments on my property?

Yes. Liens registered against your property are simply paid out of the sale proceeds at closing. Your lawyer will conduct a title search, identify all registered encumbrances, and ensure they are discharged as part of the transaction. We work with these situations routinely in Hamilton and they do not prevent a sale.

What if my home is worth less than I owe on my mortgage?

This is called being “underwater” on your mortgage, and it’s less common in Hamilton given the equity most homeowners have built up. If you are in this situation, you would need your lender’s cooperation to complete a short sale. We can discuss this scenario directly — it’s more complex but not impossible. A consumer proposal or debt consolidation may be a better first step in this case.

Facing bankruptcy and need to sell your Hamilton home fast?

Or call us directly: (647)-800-4508