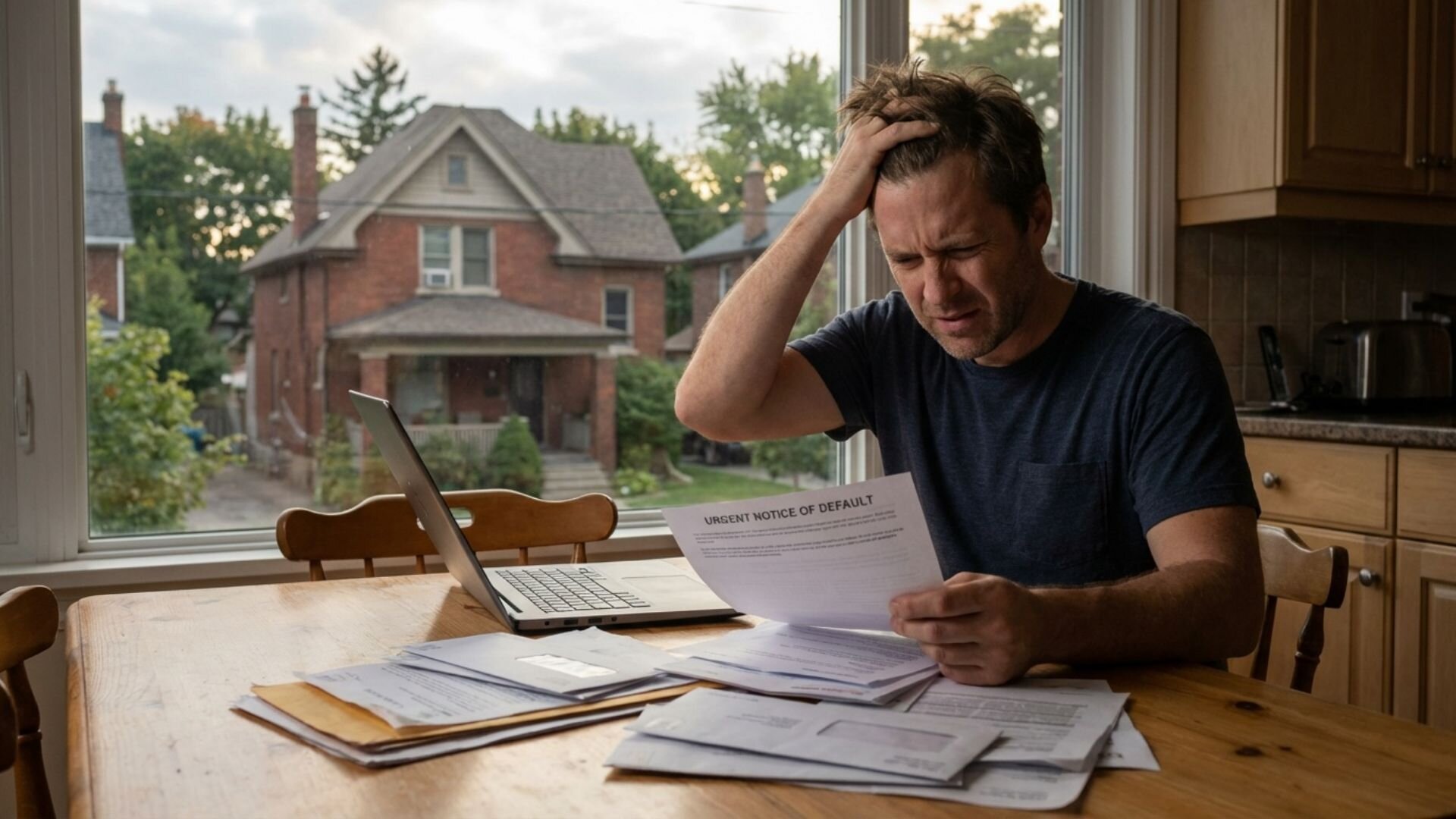

Getting a letter from your lender about power of sale is one of the most unsettling things a Hamilton homeowner can experience. Your hands shake as you read it. Your mind races. You wonder how things got to this point — and more importantly, you wonder what happens next.

The good news is that receiving a power of sale notice does not mean it’s over. You still have options, and in many cases, there is still time to act. But understanding what power of sale actually means, how the process works in Ontario, and what steps you can take right now is critical — because the clock is ticking from the moment that notice arrives.

This guide is written for Hamilton homeowners who are facing power of sale or who are worried they might be heading in that direction. We’ll walk you through everything you need to know: what it means legally, what the timeline looks like, what happens to your equity, and how selling your home before the process completes could protect more of what you’ve built.

What Is Power of Sale in Ontario?

Power of sale is a legal remedy that mortgage lenders in Ontario can use when a borrower defaults on their mortgage. It allows the lender to sell the property without going through the courts — which is why it’s different from foreclosure (a court-supervised process used more commonly in the United States and some other Canadian provinces).

In Ontario, power of sale is governed by the Mortgages Act. When a homeowner defaults on their mortgage — typically by missing payments — the lender has the right to take possession of the property and sell it in order to recover the outstanding debt. Unlike foreclosure, the lender does not take ownership of the home. Instead, they sell it on your behalf, with the proceeds going first to cover what’s owed (including principal, interest, legal fees, and penalties), and any remaining equity going back to you as the homeowner.

That last part is important: if there is equity left over after the lender recovers what they’re owed, you are entitled to it. However, in a rushed power of sale, homes are often sold quickly and not always at the best market price — which means that equity can be eroded by fees, penalties, and a below-market sale price. Acting early gives you far more control over the outcome.

How Does Power of Sale Work in Hamilton?

The power of sale process in Hamilton follows Ontario’s provincial rules under the Mortgages Act. While every situation is different, the general framework is consistent across the province. Here is what typically happens:

When you miss one or more mortgage payments, your lender will initially contact you with notices and attempts to arrange repayment. If the default continues, the lender will eventually issue a formal Notice of Sale. This document notifies you officially that they intend to exercise their power of sale and sell your property.

Once that Notice of Sale is served, you have a redemption period — typically 35 days for residential mortgages — during which you can bring the mortgage back into good standing. That means paying all arrears, accumulated interest, legal fees, and any other charges the lender has incurred. If you do this within the redemption period, the power of sale process stops.

If the redemption period expires without payment, the lender can move forward with selling the property. They are required to sell for fair market value and must apply the proceeds to the debt in a specific order: first to their costs and legal fees, then to the outstanding mortgage balance, then to any other registered encumbrances, and finally any remaining funds go back to you. If the sale proceeds don’t cover everything owed, you could be held responsible for the shortfall — called a deficiency judgment.

The Timeline: What to Expect Step by Step

One of the most important things to understand about power of sale in Hamilton is that it moves on a relatively fixed timeline. The earlier you act, the more options you have. Here’s a general breakdown of how the timeline typically unfolds:

Missed payments (Days 1–60): Most lenders won’t initiate formal power of sale proceedings after a single missed payment. They’ll send notices and attempt contact. However, some lenders will act more quickly — especially if the account has a history of late payments.

Notice of Default: Once the lender decides to proceed, they’ll issue a formal Notice of Default. This is often the first official warning that power of sale is being considered. You still have time to negotiate a repayment arrangement at this stage.

Notice of Sale Under the Mortgages Act: If the default isn’t resolved, the lender serves a formal Notice of Sale. The 35-day redemption period begins at this point. This is your last clear window to reinstate the mortgage or sell the home on your own terms.

Power of Sale proceedings (After 35 days): If the redemption period passes without resolution, the lender can retain a real estate agent, list the property, accept offers, and complete the sale — all without your direct involvement or consent.

Possession and sale: The lender may seek a court order for possession of the property and will proceed to close the sale. Once completed, the proceeds are distributed and the process ends.

The entire process from first notice to completed sale can take anywhere from a few months to over a year depending on the lender, your cooperation, and whether any legal complications arise. But waiting and hoping for the best is the most expensive strategy of all.

Why Hamilton Homeowners Fall Into Power of Sale

There is no single type of person who ends up facing power of sale. It happens to people from every background, every neighbourhood, and every income level. Life has a way of changing faster than financial plans can keep up with. Some of the most common reasons Hamilton homeowners find themselves in default include:

Job loss or reduced income: Hamilton’s manufacturing sector and broader economy have gone through significant changes over the years. A layoff, a reduction in hours, or the end of a contract can quickly turn a manageable mortgage into an impossible one.

Relationship breakdown: When couples separate, the shared income that supported the mortgage disappears. Legal costs compound the problem. What once worked for two people often becomes unworkable for one.

Health issues or disability: A serious illness, accident, or disability that prevents you from working can deplete savings quickly. Mortgage payments don’t pause because your life has been upended.

Rising interest rates: Many Hamilton homeowners who secured variable-rate mortgages or are coming up for renewal have faced dramatically higher payments. What was affordable at 2% becomes crushing at 5% or 6%.

Problem tenants or damaged property: For homeowners who depended on rental income to support their mortgage, a tenant dispute or a property left in poor condition can create cascading financial problems.

Estate or probate complications: Inherited properties sometimes come with existing mortgages or title complications that heirs weren’t expecting, leading to default before they’ve had a chance to sort out their options.

Whatever brought you here, judgment isn’t helpful — and it’s not something you’ll find from us. What matters now is understanding your options and moving quickly.

Can You Stop a Power of Sale in Hamilton?

Yes — but your ability to stop it depends largely on how early you act and which stage of the process you’re in. Here are the main ways homeowners in Hamilton have been able to halt or avoid power of sale:

Reinstate the mortgage: If you’re still within the redemption period (or before), you can bring the mortgage current by paying all arrears, interest, and fees. This completely stops the power of sale process. Your lender wants to be repaid — they do not want the hassle of selling a property. If you can raise the funds through family, a private lender, or other means, this is the cleanest solution.

Refinance: If you have equity in your home, you may be able to refinance with a new lender — even a B-lender or private mortgage — to pay out the existing mortgage and bring everything current. This buys you time to stabilize your financial situation. A mortgage broker who specializes in alternative lending can assess whether this is possible given your current situation.

Negotiate with your lender: Lenders are not eager to go through the expense and trouble of a power of sale. Many will agree to a temporary deferral, a repayment plan for arrears, or other accommodations if you contact them proactively and explain your situation. Communication is key — ignoring the problem makes it worse.

Sell the home yourself before the lender does: This is often the most underutilized — and most financially sound — option. If you sell the home before the power of sale completes, you control the sale, you can potentially maximize the proceeds, and you avoid the fees and penalties that accumulate the longer the process drags on. A fast, as-is sale to a cash buyer can close in weeks, not months.

Ready to sell your house fast in Hamilton?

Or call us directly: 647-800-4508

What Happens to the Equity in Your Home?

This is the question that worries most Hamilton homeowners facing power of sale — and rightfully so. You may have spent years building equity in your property, and the thought of losing it to fees and a below-market sale is genuinely painful.

Here’s the truth: the earlier you act, the more of your equity you protect.

When a lender completes a power of sale, they must sell for fair market value under Ontario law. However, “fair market value” in the context of a lender-managed sale doesn’t always mean the price you’d get if you spent three months preparing the home, staging it, and marketing it properly. Lenders want the sale done efficiently. They’re not motivated to wait for the best possible offer — they’re motivated to recover their money and close the file.

On top of the sale price issue, consider what gets subtracted from the proceeds before you see a dollar: outstanding mortgage balance, all accrued interest since default, legal fees for the power of sale process (which can run into the thousands), real estate agent commissions, any costs the lender incurred in preparing the property for sale, and any other registered encumbrances on the title. In a worst-case scenario — particularly if property values have softened or your mortgage is deeply in arrears — a homeowner can walk away from a power of sale with very little, or even face a deficiency if the sale doesn’t cover what’s owed.

Selling on your own terms, even in a difficult market, typically results in a better net outcome. You can choose who you sell to, negotiate the price, and control the timeline. If you’re dealing with selling in a slower market, working with a direct buyer who doesn’t require financing conditions or lengthy closing periods puts money in your pocket faster and avoids the compounding costs of a lender-managed sale.

Selling Your Home Before Power of Sale Completes

Many Hamilton homeowners don’t realize they retain the right to sell their property right up until the moment the lender completes their own sale. Even after a Notice of Sale has been issued, you can list your home, accept an offer, and close — as long as the sale completes before the lender’s process does.

This is a critical window of opportunity. Selling before the lender does gives you:

Control over the price: You’re not at the mercy of a lender who wants the quickest resolution, not the highest price. You can negotiate.

Control over the timeline: You can work with a buyer who is flexible on closing — perhaps giving you time to find alternate housing — rather than being forced out on the lender’s schedule.

Avoidance of additional fees: The longer the power of sale drags on, the more legal fees and administrative costs accumulate — all of which come out of your equity. Selling quickly stops the clock on those charges.

Protection of your credit: A completed power of sale has significant negative impact on your credit report and stays for years. A voluntary sale, even a distressed one, is treated very differently by credit bureaus and future lenders.

Many of our clients come to us having already received a Notice of Sale. Some come just days before their redemption period expires. The important thing is that they called. In most cases, we’re able to move quickly enough to give them real options — and to help them avoid the worst outcomes of a lender-managed sale.

If your home needs repairs or has deferred maintenance that’s been making you nervous about listing on the open market, know that we buy homes as-is, regardless of condition. There’s no need to spend money you don’t have on renovations before a sale — we handle all of that after closing.

Why a Cash Buyer Can Be Your Best Option in Power of Sale

When time is short and every week costs you more money in interest and penalties, the traditional real estate process can feel impossible. Listing with an agent, waiting for the right buyer, surviving inspection conditions, waiting for mortgage approval — in a power of sale situation, each of these steps carries the risk of falling through or running out of time.

A direct cash sale eliminates most of those risk factors. There are no financing conditions to worry about — we use our own funds. There are no inspection contingencies that allow a buyer to renegotiate or walk away. The timeline is predictable because we control our own closing process.

For homeowners who need to avoid a realtor commission while keeping more equity in their pocket, a cash buyer also removes that cost from the equation. If you’re researching your options, our guide on selling your house fast in Hamilton without a realtor explains the full comparison in detail — including when a direct sale makes the most financial sense and when the traditional route might serve you better.

Speed matters enormously in power of sale situations. A cash offer can often be made within 24 to 48 hours of your initial conversation with us. A closing date can be set within days or weeks — not months. In many cases, that speed is the difference between protecting your equity and losing it to the process.

How Hamilton House Buyers Helps Homeowners in Power of Sale

We’ve worked with many Hamilton homeowners who were facing power of sale, and what we’ve learned is that no two situations are identical. The details matter — how much equity you have, how far the process has progressed, what your mortgage balance is, whether there are other liens on the title, and what your ideal timeline looks like.

When you reach out to us, here’s how we approach it:

First, we have a no-pressure conversation to understand your situation fully. We’re not here to judge how you got here — we’re here to understand what you need and whether we can help. We’ll ask about the property, the mortgage, and the timeline you’re working with.

Next, we do our research and prepare a fair cash offer. Our offers are based on current Hamilton market values, the condition of the property, and our ability to close quickly. We’re transparent about how we arrive at our number.

If the offer works for you, we move forward at whatever pace you need. Our team works directly with lawyers and can coordinate with lenders to ensure the sale proceeds correctly and that any mortgage arrears are discharged at closing from the sale proceeds. We handle the paperwork and the complexity — you focus on your next chapter.

We’ve helped Hamilton homeowners in power of sale walk away with equity they would have lost if the lender had completed the sale. We’ve helped people avoid the credit damage of a completed power of sale. And we’ve helped families buy themselves time to find housing, settle their affairs, and move forward with dignity.

We can’t promise we’re the right solution for every situation — sometimes refinancing or reinstating the mortgage makes more sense. But we will always give you an honest assessment, and if a cash sale doesn’t serve your interests better than your alternatives, we’ll tell you that.

Ready to sell your house fast in Hamilton?

Or call us directly: 647-800-4508

Frequently Asked Questions About Power of Sale in Hamilton

How many mortgage payments do I need to miss before power of sale starts?

Most Ontario lenders will initiate power of sale proceedings after three or more missed payments, though technically a lender can act after a single payment default. In practice, most lenders will attempt to contact you and negotiate first. However, some lenders — particularly private lenders — may act more quickly. Don’t wait to see how long it takes: contact your lender proactively the moment you know you’ll miss a payment.

Can I sell my house during power of sale in Ontario?

Yes. As the registered owner, you retain the right to sell your property until the lender’s sale actually closes. Even if you’ve received a formal Notice of Sale, you can accept an offer from a buyer and complete the transaction — as long as it closes before the lender’s sale does. This is one of the most important facts for distressed homeowners to know.

What happens if the power of sale doesn’t cover my full mortgage?

If the lender sells the property and the proceeds don’t fully cover the outstanding mortgage balance plus fees, you may be liable for the shortfall — known as a deficiency judgment. This is another reason why taking control of your own sale, at a price you have input on, is often a better financial outcome than allowing the lender to sell.

Does power of sale affect my credit score?

Yes, significantly. A completed power of sale is reported to credit bureaus and can affect your credit rating for years, making it difficult to qualify for future mortgages or credit. Selling the property voluntarily — even in a distressed situation — is treated differently and typically has less severe long-term credit consequences.

How long does the power of sale process take in Ontario?

The minimum is around 35 days from the Notice of Sale to the lender’s right to sell, but the full process — including listing, finding a buyer, and closing — typically takes several months. In some contested cases, it can take longer. However, the costs (interest, legal fees, penalties) continue to accumulate throughout the process, so acting early almost always produces a better financial result.

Can I get my home back after power of sale starts?

During the redemption period (35 days for residential mortgages after the Notice of Sale), you can reinstate the mortgage by paying all arrears, interest, and costs in full. After the redemption period expires, it becomes much harder — you would generally need to complete a sale yourself or negotiate directly with the lender. Once the lender’s sale closes, the property is gone.

Do I need a lawyer to sell during power of sale?

Yes, you should have a lawyer involved in any real estate transaction — but particularly in a power of sale situation where there are mortgage arrears, potential liens, and other legal complexities to manage. When you sell to Hamilton House Buyers, we work directly with your lawyer (or can refer you to one) to ensure the transaction is handled properly and that all debts are discharged correctly at closing.

Is Hamilton House Buyers able to help if I’m only a few weeks from the redemption period expiring?

We will always do our best to help, regardless of where you are in the process. We’ve worked with homeowners in extremely tight timelines. The sooner you reach out, the more options we have — but please don’t assume it’s too late. Call us and let’s see what’s possible. Even if we can’t complete a full sale in time, we may be able to help you explore other options.